Wind and Hail Deductibles in Texas: Why Your Roof Claim May Cost More Than You Expect

“I have insurance.”

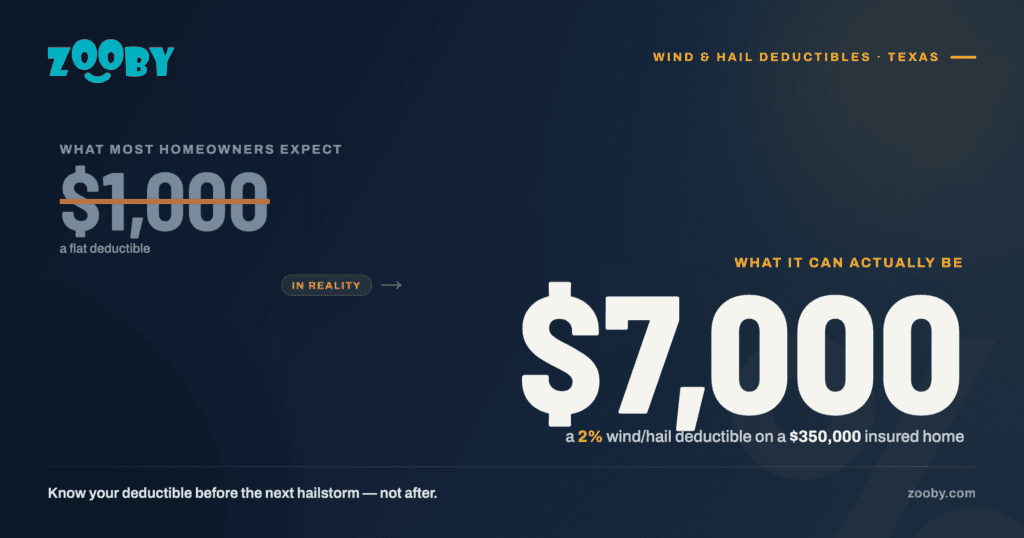

That sentence gives many homeowners peace of mind, but it does not always mean a roof repair will feel affordable after a storm.

In Texas, some homeowners have wind or hail deductibles that are based on a percentage of the home’s insured value. That means the deductible is not always a small flat fee. It can be several thousand dollars.

For a San Antonio homeowner with a $350,000 insured home and a 2% wind or hail deductible, the out-of-pocket amount could be $7,000 before insurance coverage applies.

That is why homeowners should know their deductible before the next hailstorm, not after.

Zooby helps San Antonio homeowners understand the roofing side of that decision. That starts with an inspection. From there, Zooby can help determine whether the roof needs repair, whether it may qualify for Zoobification, or whether replacement is the more responsible choice.

ZoobificationTM is Zooby’s roof rejuvenation option for qualifying asphalt shingle roofs that are aging but not beyond saving. It is not for every roof, and it should only be considered after the roof has been inspected.

What is a roof insurance deductible?

A deductible is the amount the homeowner pays before the insurance company pays on a covered claim.

The Texas Department of Insurance says a deductible may be a specific dollar amount or a percentage. TDI also shows why percentage deductibles matter. In its example, a 5% deductible on a $150,000 home amounts to $7,500. If roof repairs cost $6,500, the policy would not pay because the repair cost is less than the deductible. (Texas Department of Insurance)

This matters because a percentage can sound small until you calculate it.

One percent of a $350,000 insured home is $3,500.

Two percent is $7,000.

Three percent is $10,500.

That money may be due before the insurance company makes a contribution, depending on the policy and the claim.

Flat deductible versus percentage deductible

A flat deductible is a fixed dollar amount. For example, a homeowner may have a $1,000 deductible.

A percentage deductible is based on the home’s insured value. If the home is insured for $350,000 and the deductible is 2%, the deductible equals $7,000.

This can surprise homeowners after a storm because the deductible may end up much larger than it is.

It also changes how homeowners should think about small and moderate roof repairs. If the repair cost is below the deductible, insurance may not pay anything on that claim. If the repair cost is only slightly above the deductible, the homeowner may still end up paying most of it.

That does not mean the damage should be ignored. It means the homeowner should understand the roof condition, the deductible, and the policy before making decisions.

Why wind and hail deductibles matter after roof damage

Hail and wind can damage roofs in different ways.

Hail can bruise shingles, knock away granules, crack roofing materials, dent vents, and create weak spots that may not leak right away. Wind can lift shingles, weaken seals, bend flashing, and create openings that heavy rain later finds.

The challenge is that not every storm creates the same roofing problem. Some damage is isolated. Some damage is widespread. Some roofs were already aging before the storm. Some roofs were dry, brittle, or losing granules before hail arrived.

That is why the roof should be inspected before homeowners make assumptions about the claim.

San Antonio roofs can be weakened by heat, UV exposure, wind, hail, heavy rain, tree limbs, clogged gutters, poor attic ventilation, poor installation, foot traffic, and age. Depending on the condition of the roof, the next right step may be repair, Zoobification, or replacement.

The deductible does not answer the roofing question.

The inspection helps answer the question about the roofing.

The policy helps answer the insurance question.

Homeowners need both.

What should you check in your policy?

Start with the declarations page. This is usually the summary page that shows coverage amounts, deductibles, and important policy details.

Look for language related to wind, hail, named storm, all peril, roof damage, replacement cost, actual cash value, and percentage deductibles.

Then calculate the deductible in dollars.

If the home is insured for $350,000 and the wind or hail deductible is 2%, the deductible is $7,000.

If the home is insured for $500,000 and the deductible is 2%, the deductible is $10,000.

This is the number homeowners should know before a storm, not after a contractor or adjuster is already involved.

Replacement cost versus actual cash value

Deductibles are not the only thing homeowners should understand.

Roof coverage can also differ based on whether the policy pays replacement cost or actual cash value. The Texas Department of Insurance says replacement cost coverage pays to repair or replace property at current prices, while actual cash value coverage subtracts depreciation for age and wear. (Texas Department of Insurance)

That difference can matter after hail or wind damage, especially for older roofs.

A homeowner should not assume every policy pays the same way—the policy language matters. The roof’s age and condition may matter. The deductible definitely matters.

Should you file a roof claim if damage is below the deductible?

Not every situation is the same, and homeowners should speak with their insurance agent or carrier about policy questions.

From a roofing standpoint, the first step is understanding the condition of the roof. A roof inspection can help identify visible damage, likely repair scope, and whether the roof may be a candidate for repair, Zoobification, or replacement.

From an insurance standpoint, the deductible matters.

If the repair cost is below the deductible, the carrier may not pay anything on that claim. TDI’s example shows this clearly: if the deductible is $7,500 and the roof repair is $6,500, the policy would not pay because the repair is less than the deductible. (Texas Department of Insurance)

This is one reason homeowners should avoid guessing.

Know the roof condition. Know the deductible. Then make a more informed decision.

Can a contractor waive my deductible in Texas?

NO.

The Texas Department of Insurance says it is illegal for contractors to waive a deductible or help homeowners avoid paying it. TDI also warns that contractors may not offer to waive, rebate, or absorb a property policyholder’s deductible. (Texas Department of Insurance)

This is important after a storm.

If someone offers to “cover” your deductible, that is not a harmless favor. It can create legal and insurance problems.

A better approach is to work with a roofing company that gives clear inspections, honest recommendations, and straightforward pricing.

Where Zooby fits

Zooby does not decide whether your insurance company pays a claim.

Zooby can inspect the roof, document visible conditions, and help you understand the roofing side of the decision.

After inspection, Zooby can help determine whether the right next step may be repair, Zoobification for a qualifying roof, or replacement when the roof is no longer a good candidate for repair or rejuvenation.

Zoobification is designed for roofs with remaining useful life. If the roof qualifies, rejuvenation may be a responsible option. If it does not qualify, homeowners need a clear answer before spending money on the wrong solution.

That is the kind of clarity homeowners need before and after storm season.

What should San Antonio homeowners do before the next storm?

First, inspect the roof.

Do not rely only on what you can see from the driveway. A roof can have lifted shingles, granule loss, cracked pipe boots, weak flashing, or hail bruising that is not obvious from the ground.

Second, review the policy.

Find the deductible and calculate it in dollars. If it is a percentage deductible, write down the actual number.

Third, understand your options.

If damage is limited, repair may be enough. If the roof is aging but still has life left, Zoobification may be worth discussing if the roof qualifies. If the roof is too damaged or too brittle, replacement may be the responsible choice.

Fourth, ask about financing if larger roof work is needed and waiting would create a bigger risk.

The bottom line

A roof claim can cost more than homeowners expect because the deductible may be based on the home’s insured value rather than the size of the repair.

For a $350,000 insured home, a 2% deductible equals $7,000.

That is why San Antonio homeowners should not wait until after the next hailstorm to understand their roof or their policy.

Know your deductible. Inspect your roof. Understand whether repair, Zoobification, replacement, or financing makes the most sense.

Fill out our contact form or call us at (210) 526-4007 to schedule a roof inspection with Zooby today.

Frequently Asked Questions

What is a wind-and-hail deductible in Texas?

A wind or hail deductible is the amount the homeowner pays before insurance pays on a covered wind or hail claim. It may be a flat dollar amount or a percentage of the home’s insured value.

How much is a 2% deductible on a $350,000 home?

A 2% deductible on a $350,000 insured home equals $7,000.

Can a contractor waive my deductible in Texas?

No. The Texas Department of Insurance says it is illegal for contractors to waive your deductible or help you avoid paying it.

Should I inspect my roof before filing a claim?

Yes. An inspection helps you understand the roof’s visible condition, likely repair needs, and whether repair, Zoobification, or replacement should be considered.

What is Zoobification?

Zoobification is Zooby’s roof rejuvenation option for qualifying asphalt shingle roofs that are aging but not beyond saving. It is one possible option after inspection, not a fit for every roof.

Does Zooby decide whether my claim is covered?

No. Zooby can inspect roof condition and document visible damage. The insurance company determines coverage.

What is actual cash value roof coverage?

Actual cash value coverage pays less if the roof is older or showing wear. Replacement cost coverage may pay up to the full current cost to repair or replace the roof, depending on the policy terms.

Jeffrey Eisenberg is a renowned optimization expert and co-author of the NY Times bestselling marketing books, such as “Call to Action” and “Waiting For Your Cat To Bark.” He co-invented the Persuasion Architecture framework, helping companies increase sales by over $1 billion. Jeffrey has trained and coached hundreds of companies, including Google, NBC Universal, and HPE, by optimizing their customer experience and sales processes using data-driven strategies. He excels at anticipating customer needs and driving innovation.