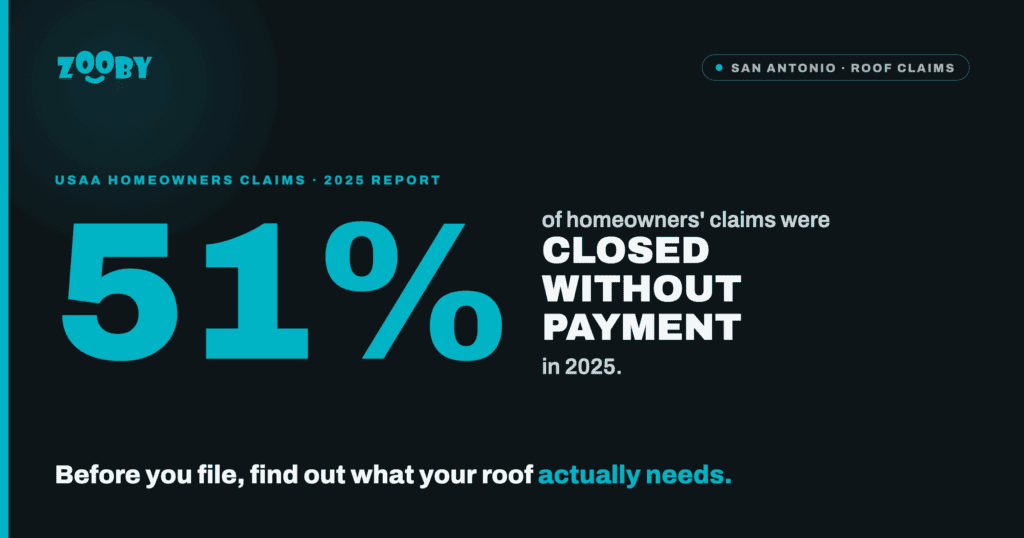

USAA Closed 51% of Homeowners’ Claims Without Payment. Before You File, Find Out What Your Roof Actually Needs.

A recent report found that USAA closed about 51% of its homeowners’ claims without making a payment in 2025.

For San Antonio homeowners, that number is hard to ignore.

It does not mean USAA wrongfully denied half of all claims. A claim can close without payment for several reasons. The estimated damage may fall below the deductible. The policy may exclude the damage. The homeowner may decide not to continue. Multiple claims may be combined, or a closed claim may be reopened later.

Still, the number reveals something every homeowner should understand before the next hailstorm.

Filing a roof claim does not guarantee that the insurance company will pay.

You can have real storm damage and still receive nothing if the approved repair cost falls below your deductible.

You can file because you believe the roof needs replacement, only to learn that the damage is repairable.

You can also create a claim record before you know whether the loss is large enough to justify filing in the first place.

That is why the smartest first step is not automatically calling the insurance company.

Before you file a claim, find out whether the roof is actually damaged, whether it can be repaired, and whether the likely cost would fall below your deductible.

What the 51% figure really tells homeowners

The headline sounds like half of USAA’s homeowners claims were rejected.

That is not necessarily what happened.

“Closed without payment” is a reporting category. It describes the outcome of the claim but does not explain why.

A claim may close without payment because:

- The repair estimate is lower than the deductible.

- The policy does not cover the cause of damage.

- The homeowner withdraws the claim.

- The insurer combines related claims.

- The damage is attributed to wear, deterioration or maintenance.

- The claim closes, then is reopened.

USAA has said that after accounting for these situations, fewer than 6% of its homeowners claims were denied without payment.

The available regulatory data do not provide sufficient detail for an external reader to independently confirm the adjusted figure. Still, the distinction matters.

A claim that closes without payment is not always a wrongful denial.

For the homeowner, however, the practical result is the same. No check arrives, and the roof may still need work.

Your deductible may decide the outcome before the claim begins

Many San Antonio homeowners have a separate wind and hail deductible.

These deductibles are often based on a percentage of the home’s insured value rather than a fixed dollar amount.

Consider a home insured for $400,000.

A 1% wind and hail deductible equals $4,000.

A 2% deductible equals $8,000.

A 3% deductible equals $12,000.

Now suppose a storm causes legitimate roof damage and the insurer approves $7,000 in repairs.

If the homeowner has a 2% deductible, the approved damage falls below the $8,000 deductible. The insurer may close the claim without making a payment.

The damage can be real.

The event can be covered.

The claim can still produce nothing.

That is why homeowners should not stop at reading “2%” on the declarations page. Convert the percentage into an actual dollar amount.

That number may shape every decision that follows.

Find out what is happening on the roof before you file

After a hailstorm, homeowners often feel pressure to act immediately.

A neighbor may already have a roofing sign in the yard. Contractors may be knocking on doors. Someone may tell you that the entire neighborhood needs new roofs.

The roof may have serious damage.

It may also have isolated damage that can be repaired.

The visible signs may be related to age rather than the recent storm. The roof may even be in better condition than you fear.

Until someone inspects it, you are working from assumptions.

A professional roof inspection can help identify:

- Missing, lifted or damaged shingles

- Hail impact marks

- Damaged flashing or vents

- Exposed or compromised areas

- Signs of water intrusion

- Wear that may not be storm-related

- Areas that may be repairable

That information does not decide whether insurance coverage applies. The insurer makes that decision under the terms of the policy.

The inspection helps answer a different question first.

What does the roof actually need?

A repair may make more sense than a claim

Many homeowners assume storm damage creates only two choices.

File a claim or replace the roof.

There may be a third option.

If the damage is limited, a targeted repair may cost less than the deductible. That could include replacing damaged shingles, repairing flashing, sealing an affected area or addressing a specific leak.

Suppose an inspection identifies $3,500 in repairs and the wind and hail deductible is $8,000.

Filing a claim is unlikely to produce a payment based on those figures.

That does not mean the roof should be ignored. It means the homeowner may be better served by understanding the repair options before creating a claim record.

There are also times when full replacement is necessary. The purpose of the inspection is not to steer every homeowner toward repair.

It is to separate repairable damage from damage that truly requires replacement.

Roof age and policy language can reduce the payment further

Even when the damage exceeds the deductible, the insurance payment may be less than expected.

Some policies cover roofs at replacement cost. Others pay actual cash value, which subtracts depreciation based on age and condition.

Older roofs may also be subject to:

- Roof payment schedules

- Age-based coverage reductions

- Cosmetic damage exclusions

- Matching limitations

- Special wind and hail provisions

- Requirements for recovering depreciation

A homeowner may hear that the roof has $20,000 in damage and assume the insurer will issue a $20,000 check.

The final amount may be reduced by depreciation, the deductible and any applicable policy limitations.

This is why the roof condition and the insurance terms must be understood together.

A roofer can explain what the roof needs.

Your agent or insurer can explain how the policy may respond.

Filing a claim creates a record.

Homeowners insurance covers certain losses, and serious damage should be reported.

Still, homeowners should know that a claim can become part of their insurance history even when no payment is made.

Insurance companies may consider claims history when making decisions about premiums, discounts, renewals or future underwriting.

That does not mean homeowners should be afraid to file a legitimate claim.

It means they should understand the likely size of the loss, the roof’s condition, and the deductible before automatically filing a claim.

A hailstorm can create urgency.

Urgency should not replace information.

What Zooby can help you understand

Zooby does not determine whether an insurance company must pay a claim.

Zooby can help you understand the condition of your roof before you make that decision.

A Zooby roof inspection can document visible damage and help determine whether the roof needs repair, replacement or another form of care.

For qualifying asphalt shingle roofs with remaining useful life, Zoobification may also be an option. It is not intended to cover up storm damage or extend the life of a roof that should be replaced. Eligibility begins with an inspection.

After the inspection, you may learn that:

- The roof has serious storm damage that should be reported.

- The damage appears repairable.

- The probable repair cost is below the deductible.

- The roof has age-related wear rather than recent storm damage.

- The roof is still performing well and does not need immediate work.

Each of those findings gives you something valuable before you file.

Clarity.

What to do before filing a roof claim

Start by finding your wind and hail deductible.

Convert the percentage into dollars.

Then have the roof inspected and ask for clear documentation of any visible damage.

Compare the likely repair cost with the deductible. Review whether the roof is covered at replacement cost or actual cash value. Look for roof schedules, exclusions and age-related limitations.

Once you have those facts, you can decide whether filing a claim makes sense.

The goal is not to avoid using your insurance.

The goal is to avoid filing without knowing what you are dealing with.

The lesson behind the 51% number

The USAA data do not prove that half of all homeowners’ claims were improperly denied.

They do show that a large percentage of claims ended without a payment.

For San Antonio homeowners, the practical lesson is straightforward.

Do not assume visible damage means full replacement.

Do not assume a filed claim will produce a check.

Do not assume a small percentage deductible means a small expense.

Before you file, find out whether the roof is actually damaged, whether it may be repairable and whether the likely cost could fall below your deductible.

Call Zooby at (210) 526-4007 to schedule a roof inspection and learn what your roof actually needs before you decide on your claim.

Jeffrey Eisenberg is a renowned optimization expert and co-author of the NY Times bestselling marketing books, such as “Call to Action” and “Waiting For Your Cat To Bark.” He co-invented the Persuasion Architecture framework, helping companies increase sales by over $1 billion. Jeffrey has trained and coached hundreds of companies, including Google, NBC Universal, and HPE, by optimizing their customer experience and sales processes using data-driven strategies. He excels at anticipating customer needs and driving innovation.